2020 Year End Individual Tax Planning

This is the time to paint your overall tax picture for 2020. By developing a year-end plan, you can maximize the tax breaks currently on the books and avoid potential pitfalls. Be aware that the concepts discussed in this article are intended to provide only a general overview of year-end tax planning. It is recommended that you review your personal situation with a tax professional.

Charitable Donations

Generally, itemizers can deduct amounts donated to qualified charitable organizations, as long as substantiation requirements are met. Be aware that the TCJA increased the annual deduction limit on monetary contributions from 50% of adjusted gross income (AGI) to 60% for 2018 through 2025. Even better, the CARES Act raises the threshold to 100% for 2020.

In addition, the CARES Act authorizes an above-the-line deduction of up to $300 for monetary contributions made by a non-itemizer in 2020 ($600 for a married couple).

YEAR-END MOVE: In most cases, you should try to “bunch” charitable donations in the year they will do you the most tax good. For instance, if you will be itemizing in 2020, boost your gift giving at the end of the year. Conversely, if you expect to claim the standard deduction this year, you may decide to postpone contributions to 2021.

For donations of appreciated property that you have owned longer than one year, you can generally deduct an amount equal to the property’s fair market value (FMV). Otherwise, the deduction is typically limited to your initial cost. Also, other special rules may apply to gifts of property. Notably, the annual deduction for property donations generally cannot exceed 30% of AGI.

Note: If you donate to a charity by credit card in December—for example, you make an online contribution—you can still write off the donation on your 2020 return, even if you do not actually pay the credit card charge until January.

Family Income-Splitting

The time-tested technique of family income-splitting still works. Currently, the top ordinary income tax rate is 37%, while the rate for taxpayers in the lowest income tax bracket is only 10%. Thus, the tax rate differential between you and a low-taxed family member, such as a child or grandchild, could be as much as 27%—not even counting the 3.8% net investment income tax (more on this later).

YEAR-END MOVE: Shift income-producing property, such as securities, to family members in low tax brackets through direct gifts or trusts. This will lower the overall family tax bill. But remember that you are giving up control over those assets. In other words, you no longer have any legal claim to the property.

Also, be aware of potential complications caused by the “kiddie tax.” Generally, unearned income above $2,200 received in 2020 by a child younger than age 19, or a child who is a full-time student younger than age 24, is taxed at the top marginal tax rate of the child’s parents. (Recent legislation reverses a TCJA change on the tax treatment.) The kiddie tax could affect family income-splitting strategies at the end of the year.

Note: If there is a danger that the kiddie tax could be triggered in 2020, some of the same income deferral strategies that are available to adults may be used for dependent children. For example, you may arrange for a child to postpone a large capital gain from a securities sale to 2021 or realize a capital loss at year-end to offset previous capital gains (see our financial planning article here).

Higher Education Expenses

The tax law provides tax breaks to parents of children in college, subject to certain limits. This often includes a choice between one of two higher education credits and a tuition-and-fees deduction.

YEAR-END MOVE: When appropriate, pay qualified expenses for next semester by the end of this year. Generally, the costs will be eligible for a credit or deduction in 2020, even if the semester does not begin until 2021.

Typically, you can claim either the American Opportunity Tax Credit (AOTC) or the Lifetime Learning Credit (LLC). The maximum AOTC of $2,500 is available for qualified expenses of each student, while the maximum $2,000 LLC is claimed on a per-family basis. Thus, the AOTC is usually preferable. Both credits are phased out based on modified adjusted gross income (MAGI).

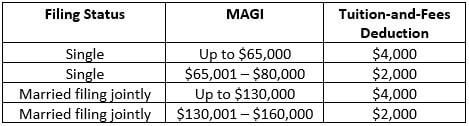

Alternatively, you may claim the tuition-and-fees deduction, which is either $4,000 or $2,000 before it is phased out based on MAGI, as shown below

Note: The tuition-and-fees deduction, which has expired and been revived several times, is scheduled to end after 2020, but could be reinstated again by Congress.

Note: The tuition-and-fees deduction, which has expired and been revived several times, is scheduled to end after 2020, but could be reinstated again by Congress.

Medical & Dental Expenses

Previously, taxpayers could only deduct unreimbursed medical and dental expenses above 10% of their AGI. However, the TCJA temporarily lowered the threshold to 7.5% of AGI for 2017 and 2018. Subsequent legislation extended this tax break through 2020.

YEAR-END MOVE: When it is possible, accelerate non-emergency expenses into this year to benefit from the lower threshold. For instance, if you expect to itemize deductions and have already surpassed the 7.5%-of-AGI threshold this year, or you expect to clear it soon, accelerate elective expenses into 2020. Of course, the 7.5%-of-AGI threshold may be extended again, but you should maximize the tax deduction when you can.

To qualify for a deduction, the expense must be for the diagnosis, cure, mitigation, treatment or prevention of disease or payments for treatments affecting any structure or function of the body. Any costs for your general health or well-being are nondeductible.

Note: Don’t forget to count unreimbursed medical and dental expenses you have paid for your immediate family members, as well as other tax dependents such as an elderly parent or in-law. These extra expenses can push you over the 7.5%-of-AGI mark for the year or boost an existing deduction.

Estimated Tax Payments

The IRS requires you to pay federal income tax through any combination of quarterly installments and tax withholding. Otherwise, it may impose an “estimated tax” penalty.

YEAR-END MOVE: No estimated tax penalty is assessed if you meet one of these three “safe harbor” exceptions under the tax law.

1. Your annual payments equal at least 90% of your current liability;

2. Your annual payments equal at least 100% of the prior year’s tax liability (110% if your AGI for the prior year exceeded $150,000); or

3. You make installment payments under an “annualized income” method. This option may be available to taxpayers who receive most of their income during the holiday season.

Note: If you have received unemployment benefits in 2020—for example, if you lost your job due to the COVID-19 pandemic—remember that those benefits are subject to income tax. Factor this into your estimated tax calculations for the year.

Miscellaneous

* Watch out for the alternative minimum tax (AMT). The AMT applies if a separate complex calculation involving “tax preference items” and certain adjustments exceeds your regular tax liability. Have an assessment of your AMT liability made to determine your year-end approach.

* Make home improvements that qualify for mortgage interest deductions as acquisition debt. This includes loans made to substantially improve your principal residence or one other home. Note that the TCJA suspended deductions for home equity debt for 2018 through 2025.

* With a Section 529 plan, you can set up an account for a child’s college education that can grow without any current tax erosion. Distributions used to pay for qualified expenses are exempt from tax. Beginning in 2018, the TCJA expanded the use of 529 plans for tuition payments of up to $10,000 a year for a child’s kindergarten, elementary or secondary school education.

* Consider the tax impact of a divorce or separation. The TCJA repealed the deduction for alimony expenses for payers and the corresponding inclusion in income for recipients, for divorce and separation agreements executed after 2018. Note that deductions may still be available for pre-2019 agreements that are modified after 2018.

* Meet student loan obligations. Under the CARES Act, payment on many student loans was suspended tax-free until September 30 and then through December 31 by an executive order. Barring any further developments, you must resume required payments in 2021.

* If you own property that was damaged in a federal disaster area in 2020, you may qualify for quick casualty loss relief by filing an amended 2019 return. The TCJA suspended the deduction for casualty losses for 2018 through 2025, but retained a current deduction for disaster-area losses.

Conclusion

This year-end tax-planning article is based on the prevailing federal tax laws, rules and regulations. Of course, it is subject to change, especially if additional tax legislation is enacted by Congress before the end of the year.

You may be interested in the other year-end articles:

- Click here for the 2020 Year-End Business Tax Planning article

- Click here for the 2020 Year-End Financial Tax Planning article

Finally, remember that this article is intended to serve only as a general guideline. Your personal circumstances will likely require careful examination. We would be glad to schedule a meeting with you to assist with all your tax-planning needs.