2020 Financial Year End Tax Planning

This is the time to paint your overall tax picture for 2020. By developing a year-end plan, you can maximize the tax breaks currently on the books and avoid potential pitfalls. Be aware that the concepts discussed in this article are intended to provide only a general overview of year-end tax planning. It is recommended that you review your personal situation with a tax professional.

Capital Gains and Losses

Frequently, investors time sales of assets like securities at year-end to produce optimal tax results. For starters, capital gains and losses offset each other. If you show an excess loss for the year, it offsets up to $3,000 of ordinary income before being carried over to the next year. Long-term capital gains from sales of securities owned longer than one year are taxed at a maximum rate of 15% or 20% for certain high-income investors. Conversely, short-term capital gains are taxed at ordinary income rates reaching up to 37% in 2020.

YEAR-END MOVE: Review your investment portfolio. Depending on your situation, you may harvest capital losses to offset gains realized earlier in the year or cherry-pick capital gains that will be partially or wholly absorbed by prior losses.

Be aware of even more favorable tax treatment for certain long-term capital gains. Notably, a 0% rate applies to taxpayers below certain income levels, such as a young child. Furthermore, some taxpayers who ultimately pay ordinary income tax at higher rates due to their investments may qualify for the 0% tax rate on a portion of their long-term capital gains.

However, watch out for the “wash sale rule.” If you sell securities at a loss and reacquire substantially identical securities within 30 days of the sale, the tax loss is disallowed. A simple way to avoid this harsh result is to wait at least 31 days to reacquire substantially identical securities.

Note: The 0%/15%/20% rate structure for long-term capital gains also applies to qualified dividends you have received in 2020. These are dividends paid by U.S. companies or qualified foreign companies.

Net Investment Income Tax

In addition to capital gains tax, a special 3.8% tax applies to the lesser of your “net investment income” (NII) or the amount by which your modified adjusted gross income (MAGI) for the year exceeds $200,000 for single filers or $250,000 for joint filers. (These thresholds are not indexed for inflation.) The definition of NII includes interest, dividends, capital gains and income from passive activities, but not Social Security benefits, tax-exempt interest and distributions from qualified retirement plans and IRAs.

YEAR-END MOVE: Assess the amount of your NII and your MAGI at the end of the year. When it is possible, reduce your NII tax liability in 2020 or avoid it altogether.

For example, you might add municipal bonds (“munis”) to your portfolio. Interest income generated by munis does not count as NII, nor is it included in the calculation of MAGI. Similarly, if you turn a passive activity into an active business, the resulting income may be exempt from the NII tax. These rules are complex, so obtain professional assistance.

Note: When you add the NII tax to your regular tax plus any applicable state income tax, the overall tax rate may approach or even exceed 50%. Factor this into your investment decisions.

Required Minimum Distributions

As a general rule, you must receive “required minimum distributions” (RMDs) from qualified retirement plans and IRAs after reaching age 72 (70½ for taxpayers affected prior to 2020). The amount of the RMD is based on IRS life expectancy tables and your account balance at the end of last year. If you do not meet this obligation, you owe a tax penalty equal to 50% of the required amount (less any amount you have received) on top of your regular tax liability.

YEAR-END MOVE: Take RMDs in 2020 if you need the cash. Otherwise, you can skip them this year, thanks to a suspension of the usual rules by the CARES Act. There is no requirement to demonstrate any hardship relating to the pandemic.

However, if you already received an RMD this year and did not return the money to a qualified plan or IRA by August 31, the distribution is generally taxable in 2020.

Typically, retirees wait until late in the year to arrange RMDs. If you still intend to take any of your RMDs in 2020, make sure you complete the arrangements in time to have this accommodated by the financial institution.

Note: RMDs are not treated as NII for purposes of the 3.8% tax. Nevertheless, an RMD may still increase your MAGI used in the NII tax calculation.

IRA Rollovers

If you receive a distribution from a qualified retirement plan or IRA, it is generally subject to tax unless you roll it over into another qualified plan or IRA within 60 days. In addition, you may owe a 10% tax penalty on taxable distributions received before age 59½. However, some taxpayers may have more leeway to avoid tax liability in 2020 under a special CARES Act provision.

YEAR-END MOVE: Take your time redepositing the funds if it qualifies as a COVID-19 related distribution. The CARES Act gives you three years, instead of the usual 60 days, to redeposit up to $100,000 of funds in a plan or IRA without owing any tax.

To qualify for this tax break, you (or your spouse, if you are married) must have been diagnosed with COVID-19 or experienced adverse financial consequences due to the virus (e.g., being laid off, having work hours reduced or being quarantined or furloughed). If you do not replace the funds, the resulting tax is spread evenly over three years.

Note: This may be a good time to consider a conversion of a traditional IRA to a Roth IRA. With a Roth, future payouts are generally exempt from tax, but you must pay current tax on the converted amount. Have a tax professional help you determine if this makes sense for your situation.

Estate and Gift Taxes

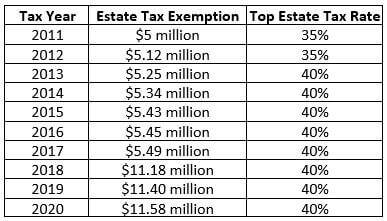

Since the turn of the century, Congress has gradually increased the federal estate tax exemption, while eventually establishing a top estate tax rate of 40%. At one point, the estate tax was repealed—but only for 2010—while the unified estate and gift tax exclusion was severed and then subsequently reunified.

Finally, the TCJA doubled the exemption from $5 million to $10 million for 2018 through 2025, inflation-indexed to $11.58 million in 2020. The following table shows the progression of the estate tax exemption and top estate tax rate during the last decade.

YEAR-END MOVE: Update your estate plan to reflect current law. For instance, you may revise wills and trusts to accommodate the rule allowing portability of the estate tax exemption.

Under the “portability provision” for a married couple, the unused portion of the estate tax exemption of the first spouse to die may be carried over to the estate of the surviving spouse. This tax break is now permanent, so incorporate it into your estate planning decisions.

Note: With the gift tax exclusion, you can give each recipient, like a young family member, up to $15,000 in 2020 without paying any federal gift tax. This exclusion is effectively doubled to $30,000 for joint gifts made by a married couple. These gifts reduce the size of your taxable estate.

Miscellaneous

* Contribute up to $19,500 to a 401(k) in 2020 ($26,000 if you are age 50 or older). If you clear the 2020 Social Security wage base of $137,700 and promptly allocate the payroll tax savings to a 401(k), you can increase your deferral without any further reduction in your take-home pay.

* Sell real estate on an installment basis. For payments over two years or more, you can defer tax on a portion of the sales price. Also, this may effectively reduce your overall tax liability.

* Invest in passive income generators (PIGs). Generally, you can only use losses from passive activities (e.g., most real estate investments) to offset income from other passive activities, with limited exceptions. With a PIG, you can absorb more of your passive activity losses.

* From a tax perspective, it is often beneficial to sell mutual fund shares before the fund declares dividends (the ex-dividend date) and buy shares after the date the fund declares dividends.

* Consider a qualified charitable distribution (QCD). If you are age 70½ or older, you can transfer up to $100,000 of IRA funds directly to a charity. Although the contribution is not deductible, the QCD is exempt from tax. This may benefit your overall tax picture.

Conclusion

This year-end tax-planning article is based on the prevailing federal tax laws, rules and regulations. Of course, it is subject to change, especially if additional tax legislation is enacted by Congress before the end of the year.

You may be interested in the other year-end articles:

- Click here for the 2020 Year-End Individual Tax Planning article

- Click here for the 2020 Year-End Business Tax Planning article

Finally, remember that this article is intended to serve only as a general guideline. Your personal circumstances will likely require careful examination. We would be glad to schedule a meeting with you to assist with all your tax-planning needs.