Considerations for Business Entity Selection Under Tax Reform

By Vince Tomei | Partner and Department Head, Tax and Business Services

C Corporation or S Corporation? It All Depends.

Ever since Congress enacted the Tax Cuts and Jobs Act in December, many business owners are reconsidering which business entity makes the most sense for their particular business. With the new, lower tax rate for C corporations, many pass-through entities, including S corporations, are reconsidering their structure to take advantage of the substantially reduced 21% corporate tax rate.

The Act also provided tax relief to S corporations (and other pass-through entities) in the form of a temporary business income deduction (with some limitations), so that’s what makes it complicated. It may not be worth switching after all. When it comes to choosing business entities, one thing hasn’t changed—it all depends on a number of factors.

Calculating Benefits of New Flat Tax and Business Income Deduction

Tax reform has dramatically reduced the effective tax rates on business income for all businesses, including C corporations and pass-through entities. The new 21% flat rate for C corporations applies to both income and gain on the sale of assets. For many pass-through entities structured as limited liability companies or S corporations, the flat tax rate is very attractive, and that has raised the question of whether they should convert to a C corporation for tax relief.

For many S corporation business owners, the real tax break may be the 20% new qualified business income deduction for pass-through entities against their flow-through income. Specifically, for tax years beginning after Dec. 31, 2017, the new 20% deduction would be allowed for taxpayers who have domestic “qualified business income” from a pass-through or sole proprietorship engaged in a “qualified trade or business.”

A “qualified trade or business” means any trade or business income other than a specified trade or business, with an exception for engineering and architecture services, or the trade or business of performing services as an employee. Examples of those businesses excluded from the 20% business income deduction include law firms, consulting businesses and accounting firms.

Determining the effective tax rate for S corporations and partnerships has traditionally been a bit more complex because business taxable income is passed through to the owners who are then taxed at their marginal rate.

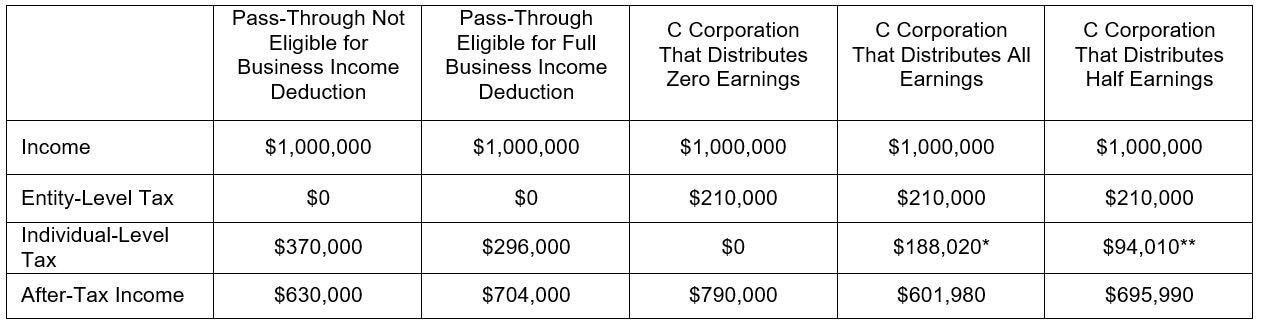

The table below illustrates the after-tax income available to a business owner based on if they are eligible for the business income deduction and for a pass-through business versus a C corporation.

(EXCLUDES STATE INCOME TAX)

(EXCLUDES STATE INCOME TAX)

* $790,000 x (20% dividend tax + 3.8% investment income tax)

** $395,000 x (20% dividend tax + 3.8% investment income tax)

As illustrated in the table above, the pass-through tax rate could range from 37% to 29.6%, depending on the type of business. The C corporation tax rate ranges from 39.8% to 21%, depending on the level of earnings distributed to owners.

Section 1202 Considerations

Section 1202 was enacted in 1993 and generally provides non-corporate taxpayers with an exemption from federal income tax for eligible gains for the sale of qualified small business stock held more than five years. Generally, the exemption is limited to $10 million per taxpayer or 10 times the taxpayer’s original adjusted basis; only applies to originally issued stock; the corporation must not have more than $50 million in aggregate gross assets at the time the stock is issued; and must be in a qualified trade or business. Individuals with stock eligible for Section 1202 treatment need to consider the potential exclusion if the stock is sold in a qualifying transaction. Depending on the particular facts, the Section 1202 exemption can far outweigh the effect of double taxation.

Looking Ahead

Business owners will need to think about their business structure in terms of their specific needs. Examples include reinvesting earnings into the company vs. paying the owners, and exit plans for the near future. C corporations and LLCs are much more flexible in the type of owners they can have when compared to S corporations. A C corporation can enjoy the low 21% tax rate as long as it doesn’t plan on distribution earnings to owners, which would trigger the double tax. In addition, if there is an exit plan in the near future which can typically generate large gains, the S corporation or LLC provides greater flexibility to sell either assets or stock. A sale of assets by a C corporation would be subject to double tax and thus, provide less flexibility upon exit. However, the sale of C corporation stock could meet the Section 1202 exemption.

This analysis is complex, so business owners should consult with their qualified tax advisors and legal counsel to assist in making a determination regarding whether or not to change their business structure.

Do you need help determining the best approach for your business structure? Contact us today!

About Vince Tomei: Vince is a Partner and Department Head of the Tax and Business Services department. He has been with the firm for over 25 years and has accounting experience working in many areas of industry including construction, manufacturing, real estate, retail and medical professional. He also works closely with high wealth individuals relative to tax and estate planning.